Part 1: Remedying the Site-of-Service Premium

Medicare's Incremental Path to Site-Neutral Payment

This is the first in a series that uses two active Medicare payment changes — site-neutral payment expansion and the 340B drug payment offset — as a working illustration of a broader challenge: the need to follow, understand, and account for legislative and regulatory change in healthcare. Each policy is complex on its own. Together, they interact in ways that can produce adverse outcomes neither was designed to create. Operators of care delivery companies and architects of alternative payment models need to understand the implications and update their thinking as these changes unfold. We walk through the rate mechanics and the 340B program structure first, then show what both mean for episode cost and how they may affect value-based care arrangements. The analysis focuses on Medicare FFS — where the changes originate — with MA implications noted throughout.

Consider a Medicare patient receiving pembrolizumab (an immunotherapy to treat many types of cancer) at an infusion center two miles from the hospital that owns it. The drug is the same. The nurse is the same. The chair is the same. But because the infusion center is enrolled in Medicare as a hospital outpatient department, it bills a facility fee of $337 just for administering the infusion. At a freestanding oncology clinic with no hospital affiliation, there is no separate facility fee — the physician's all-in rate for the same service is $133. The drug cost is identical. That $204 gap exists entirely because of how the site is classified in Medicare's billing system — not what was done, not who did it.

This is the site-of-service premium. It is not a Medicare peculiarity, and it is not limited to drug administration — the same dynamic applies to E&M visits, imaging, laboratory services, and surgical procedures. Wherever a service can be billed under two different facility classifications, the hospital outpatient rate exceeds the physician office rate, often by a wide margin. It is a structural feature of how healthcare services are priced in the United States, and it exists across every payer. The incentives embedded in the billing structure reward routing care through higher-paying facility classifications — and the data reflects that. Arnold Ventures, citing CMS claims data, reports that between 2015 and 2021 chemotherapy administration billed in freestanding clinician offices declined by more than 14% while the same services in hospital outpatient departments increased by more than 21%.

The commercial version is larger and harder to fix. Milliman's 2025 benchmarking estimates commercial payers reimburse medical services at approximately 196% of fully loaded Medicare FFS rates nationally, with facility fees a primary driver in outpatient settings. Hospital systems with regional market dominance negotiate from structural strength — the credible threat to go out of network, consolidated physician workforces, and the absence of viable alternatives in many markets. Commercial facility fee premiums frequently exceed Medicare's differential and are sticky in ways regulated rates are not: changing them requires bilateral contract renegotiation on multi-year cycles, under conditions that favor hospital systems.

Even for traditional Medicare, meaningful reform requires Congress. Arnold Ventures estimates comprehensive site-neutral legislation would save Medicare more than $150 billion and reduce beneficiary costs by more than $90 billion — with 84% voter support across party lines. That scale of change is beyond what annual rulemaking can accomplish. But while Congress has not acted comprehensively, CMS has been making incremental progress within its existing authority: clinic visits at excepted off-campus provider-based departments were repriced to physician office-equivalent rates in 2019; drug administration services followed in the CY2026 OPPS final rule; on-campus hospital outpatient departments are now in scope for future rulemaking.

This post focuses on a specific set of drug administration codes under Medicare FFS, where the rate data is transparent and the policy changes are confirmed. The near-term impact on MA and commercial is limited — MA contracts renegotiate on their own cycles, and commercial contracts move even more slowly; neither automatically follows a CMS rule. But the analysis matters beyond traditional Medicare because of CMS’s benchmark role. Medicare FFS rates are the reference point around which MA contracts, Medicaid fee schedules, and commercial negotiations orient. When CMS reprices a service category, it shifts the anchor. Slowly, imperfectly — but it shifts.

Location, Location: How Medicare Pays for Outpatient Services

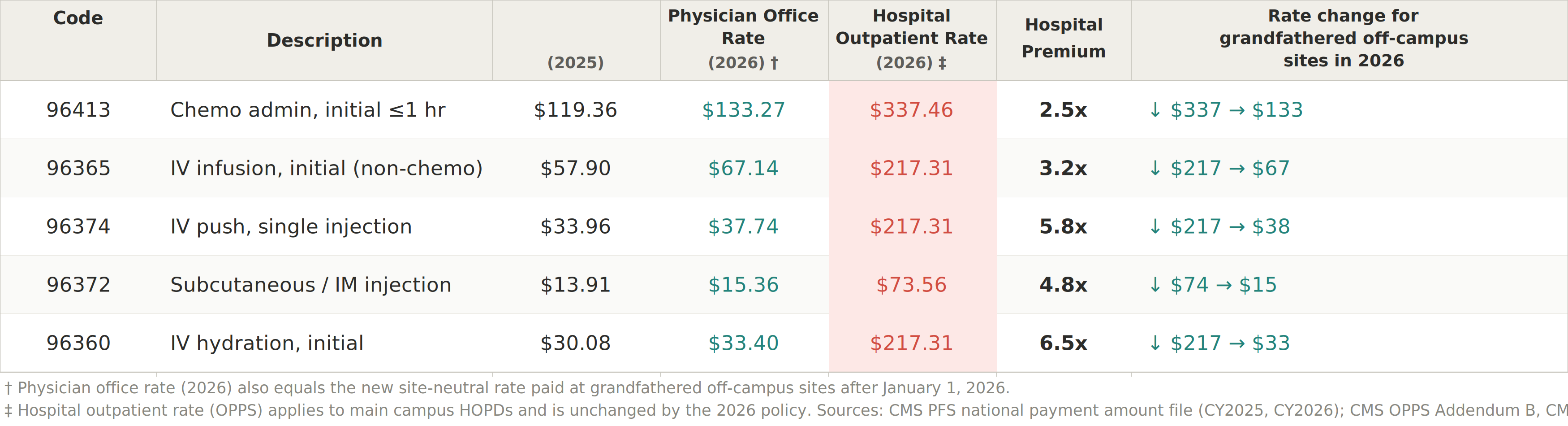

To understand where the gap comes from, it helps to know that Medicare pays for outpatient services through two completely separate rate systems depending on who owns the facility. We will use CPT 96413 — the most commonly billed drug administration code in outpatient oncology — as the running example throughout.

When a patient receives an infusion at a freestanding physician office — a clinic with no hospital affiliation — Medicare pays a single all-in rate set by the Physician Fee Schedule (PFS). That rate covers the physician's professional work, the nursing staff time, the supplies, and the overhead. There is no separate facility fee. For 96413 in 2026, that all-in rate is $133.

When the same patient receives the same infusion at a hospital outpatient department (HOPD) — whether a main campus infusion suite or an off-campus facility enrolled as part of the hospital — Medicare splits the payment across two separate billing tracks. The hospital bills a facility fee under the Outpatient Prospective Payment System (OPPS), covering the overhead of the encounter: the infusion chair, nursing staff, supplies, and facility operations. For 96413 at a main campus HOPD in 2026, that facility fee is $337. The physician also bills separately for their professional work, at the lower “facility” rate under the Physician Fee Schedule — approximately $26 — because the hospital, not the physician, is covering the overhead. Total Medicare payment for the HOPD encounter: roughly $363.

The gap between the two approaches: $363 total at the HOPD versus $133 at the freestanding office — a difference of roughly $230 for the same clinical service. The facility fee accounts for all of it. Site-neutral payment policy targets this gap specifically: it does not change the physician’s fee, and it does not change what Medicare pays for the drug. It changes only what Medicare pays the hospital for the overhead of administering the service.

The facility fee was designed to compensate hospitals for the genuine overhead of running outpatient departments — capital infrastructure, nursing and pharmacy staffing, compliance costs that freestanding offices don’t carry. That rationale has become harder to rationalize as hospital systems have been acquiring independent physician practices and operating them as outpatient departments and billing at hospital rates for encounters that are operationally unchanged from before the acquisition.

CMS has responded by trying to reflect this reality in how it pays — distinguishing between types of hospital outpatient sites and incrementally adjusting reimbursement to match the actual care delivery setting rather than just the billing classification. The approach is deliberate and layered: not a single across-the-board cut, but a series of targeted changes that treat different site types differently. That nuance is what makes this policy area genuinely complex to follow.

Three types of sites, three rate structures — and a decade of policy changes

Not all outpatient facilities billing under hospital rates are the same. Understanding the current policy requires distinguishing three types of sites, because the rules are different for each.

Main campus HOPDs are the original hospital outpatient departments — physically on or adjacent to the main hospital building. These have always billed under OPPS and continue to do so. No site-neutral payment change has touched them. A patient receiving chemotherapy at a main campus cancer infusion center is still billed at the full $337 OPPS rate in 2026.

Off-campus provider-based departments opened after November 2, 2015 are facilities that hospitals enrolled as outpatient departments after Congress drew a line in the ACA. These sites are paid at physician office-equivalent rates — the same $133 — regardless of their hospital affiliation. They never had access to the OPPS premium.

Off-campus PBDs enrolled before November 2015 — the “grandfathered” or “excepted” sites — are where the active policy changes are happening. These facilities had been billing at full OPPS rates ($337 for 96413) since their enrollment. Congress grandfathered them in 2015 rather than immediately cutting their rates. CMS has been narrowing that premium in stages:

2019: Clinic and office visits at these sites were repriced from the OPPS rate to the physician office rate. Drug administration and infusion services were left at OPPS rates.

2026: Drug administration services at these same grandfathered off-campus sites were repriced to the physician office rate. For 96413, that is a reduction from $337 to $133 per infusion visit, effective January 1, 2026.

Main campus HOPDs remain unaffected. Rural sole community hospitals are exempt from the 2026 change. And these changes apply only to drug administration service codes — imaging, radiation oncology, and other service categories at the same grandfathered sites continue to bill at full OPPS rates.

What Do the Numbers Show?

The table below shows the rate structure for the most commonly billed drug administration codes in an oncology population. The three rate columns correspond to the three site types described above.

A few things in the table are worth noting:

The physician’s payment is the same across all settings — the entire rate differential is in the hospital facility fee, not physician compensation.

The premium is largest for lower-intensity services: hydration ($33 at a physician office, $217 at a hospital) and IV push ($38 vs. $217) carry higher ratios than chemotherapy itself, because Medicare’s hospital outpatient rate-setting groups these three codes into the same payment bucket regardless of their very different physician office rates.

The 2025-to-2026 increase in physician office rates (10–16%, well above the 3.3% annual update) reflects a CMS methodology change that increased non-facility practice expense allocations — the new site-neutral rate at grandfathered off-campus sites is consequently higher in 2026 than it would have been under prior methodology, which modestly offsets the reduction from losing OPPS rates.

Several add-on codes commonly billed alongside these — 96367 (each additional infusion hour), 96375 (sequential injection add-on), 96417 (sequential chemo add-on) — are excluded from the table because they generate no separate payment under hospital outpatient billing; the hospital facility fee covers them within the primary service rate. Under the physician fee schedule they are billed and paid separately.

What Does This Mean for Cost of Care?

Building from code to episode: for a stage IV NSCLC patient on carboplatin, pemetrexed, and pembrolizumab — the standard first-line regimen in the absence of actionable mutations — a 6-month outpatient episode typically involves roughly 7 infusion visits (4 induction cycles plus 3 maintenance pembrolizumab administrations). At the 2026 rate differential of $204 per visit for 96413 alone, that is approximately $1,430 in facility fee reduction across the episode — but only at sites subject to the repricing. On a full Part A + B + D episode that typically runs $60–70k for a stage IV lung cancer patient, $1,430 represents roughly 2% of total episode spending. Not a rounding error, and concentrated entirely on the administration side of the ledger.

That 2%, however, comes with an important qualifier: it applies only at grandfathered off-campus sites, and the realized cost reduction depends on the site mix within a given geography. A patient receiving the same regimen at a main campus HOPD, or at an NCI-designated cancer center on hospital grounds, sees none of it. The impact for any VBC program depends on what share of attributed infusion volume sits at affected sites — and the exceptions and carve-outs make this genuinely difficult to calculate. Main campus HOPDs are untouched. Rural sole community hospitals are exempt. Only a specific subset of grandfathered off-campus facilities is in scope. Most programs have not mapped their attributed infusion volume to this level of site granularity, which means the actual impact on their cost of care is an open question until they do.

At the system level, CMS estimates the repricing reduces OPPS spending by $290 million annually. That breaks into two effects worth separating: $220 million is Medicare program savings — taxpayer money recovered from a program that spends over $800 billion annually. The other $70 million is reduced beneficiary coinsurance — direct out-of-pocket relief for patients currently paying 20% of the OPPS rate at affected sites.

Where Do We Go from Here?

CMS’s incremental approach is consistent with how major Medicare payment changes move — bounded steps, prospective only, with carve-outs to limit acute disruption. That caution is understandable. But it has a cost worth naming: the site-of-service differential is a real and ongoing transfer from Medicare taxpayers, commercial premium payers, and patients paying 20% coinsurance on OPPS rates they have no visibility into. Arnold Ventures puts the full scope at $150 billion in available Medicare savings and $140 billion in commercial savings through comprehensive legislation. The $290 million from the CY2026 repricing is meaningful — and a fraction of what is possible. The direction is right. The pace is a policy choice.

For MA and commercial, the gap between FFS policy and market reality is wider still. MA facility agreements renegotiate on their own multi-year cycles; a rule effective January 1, 2026 does not reset a contract signed in 2024. For commercial, the timeline is longer and hospital systems negotiate from a stronger position. The policy moves the anchor. How far and how fast the rest of the market follows is not determined by the rule.

For VBC architects and operators, this is genuinely hard — and the complexity deserves acknowledgment rather than hand-waving. The policy changes are staggered across service categories and years. Their impact is geographically uneven, because grandfathered off-campus sites are not uniformly distributed across markets. They flow into FFS benchmarks with a lag. And MA contracts sit between the FFS signal and the actual cost of care, absorbing or delaying the impact depending on when they last renegotiated. None of this is insurmountable. But it does mean that measuring the effect on your program requires deliberate infrastructure: site-type classification of attributed providers, contract-level tracking of MA facility rates, and explicit scenario modeling for the benchmark timing gap — not a one-time analysis, but ongoing as the policy continues to evolve.

There is a broader opportunity here worth flagging. CMMI operates multiple oncology and specialty programs, each with its own benchmark methodology, data infrastructure, and measurement approach. A unified infrastructure — shared site-type crosswalks, common provider classification standards, a policy change log that flows directly into benchmark adjustment models — would make it faster to design, implement, and measure payment policy changes across all of them. Right now, each program and each operator builds bespoke systems to answer the same underlying questions. That fragmentation slows the feedback loop between policy intent and measured impact. Solving that problem would help accelerate the former.

Up next: Part 2 will add the second layer: the 340B conversion factor offset, which compresses non-drug OPPS service revenue independently of where a hospital's outpatient departments are located — and, as a structural matter, lands hardest on non-340B hospitals that receive no offsetting benefit.

Key sources