Part 2: The 340B Program

A "Subsidy" Program Under Pressure

My previous post covered the site-of-service premium and what the CY2026 OPPS final rule does to it — the repricing of drug administration fees at grandfathered off-campus provider-based departments that compresses facility fee revenue on the non-drug service side of the hospital income statement. This post adds a second, unrelated compression on the same line: the 340B conversion factor offset, which arrived through a completely different statutory channel and hits a broader set of hospitals. Together, they are restructuring the revenue architecture of hospital outpatient care in ways neither was designed to create. This post explains how the offset works, who it hits, and why the CY2027 rate decision is worth modeling now.

What Is the 340B Program?

The 340B Drug Pricing Program was created by Congress in 1992 under Section 340B of the Public Health Service Act. Its design is a cross-subsidy: drug manufacturers are required to sell covered outpatient drugs to qualifying “covered entities” at ceiling prices — a statutory maximum set at average manufacturer price (AMP) minus a unit rebate amount, under a formula that differs for branded and generic drugs. Covered entities purchase at that discounted price and bill Medicare at the standard Part B rate of ASP+6%. The spread between acquisition cost and reimbursement — the 340B margin — flows to the covered entity. The subsidy is not a federal appropriation; it is effectively a transfer from manufacturers to safety-net providers, with Medicare as the billing vehicle.

Qualifying covered entity categories include disproportionate share hospitals, children’s hospitals, critical access hospitals, federally qualified health centers, rural referral centers, and freestanding cancer hospitals. The program was designed to let these providers stretch limited resources further — serving low-income and uninsured patients at a lower net drug cost than the open market would allow.

The program’s scale has grown well beyond what Congress contemplated in 1992. Total covered entity drug purchases under 340B reached $81.4 billion in 2024, with disproportionate share hospitals alone accounting for $64.1 billion. Specialty medicines — primarily oncology and immunology — drove most of that growth, consistent with national drug spending trends. But the growth is not only about drug prices. As hospitals acquire physician practices and enroll them as provider-based departments — the same dynamic described in my previous post — those sites can qualify under the acquiring hospital’s covered entity status, extending 340B purchasing eligibility to outpatient settings that may serve a materially different patient population than the safety-net mission intended. The result is a program whose financial footprint has grown substantially faster than its target population, and that gap is the source of most of the sustained policy friction.

The 340B margin is meaningful wherever high-cost outpatient drugs are administered — oncology, rheumatology, ophthalmology, neurology. The economic logic follows the drug cost, not the disease category: four of the top ten 340B drugs by 2024 purchase volume are oncology agents, but the other six span HIV, multiple sclerosis, and immunology. I work in oncology, and it represents the largest single chunk of the program — pembrolizumab alone was $8.16 billion in 340B purchases in 2024, more than any other drug and not particularly close.

Medicare’s Failed Attempted Fix

Starting in calendar year 2018, CMS reduced the Medicare Part B payment rate for 340B-acquired drugs from ASP+6% to ASP-22.5%. The rationale was direct: 340B hospitals acquire drugs at prices well below market, their actual acquisition cost is substantially below what ASP+6% represents, and the spread constitutes windfall revenue rather than necessary program support. CMS argued it had authority under the OPPS statute to set payment rates for separately payable drugs using data other than ASP.

The hospital industry challenged the cut. In American Hospital Association v. Becerra, decided June 2022, the Supreme Court reversed CMS unanimously. The statutory problem was precise: the OPPS statute permits CMS to deviate from the ASP+6% default only under two conditions — either pay ASP+6%, or conduct a survey of hospitals’ actual acquisition costs and set rates based on that survey. CMS had done neither. It had estimated acquisition costs without the required survey and imposed a cut on that basis. Nine justices agreed that was impermissible — not a close call.

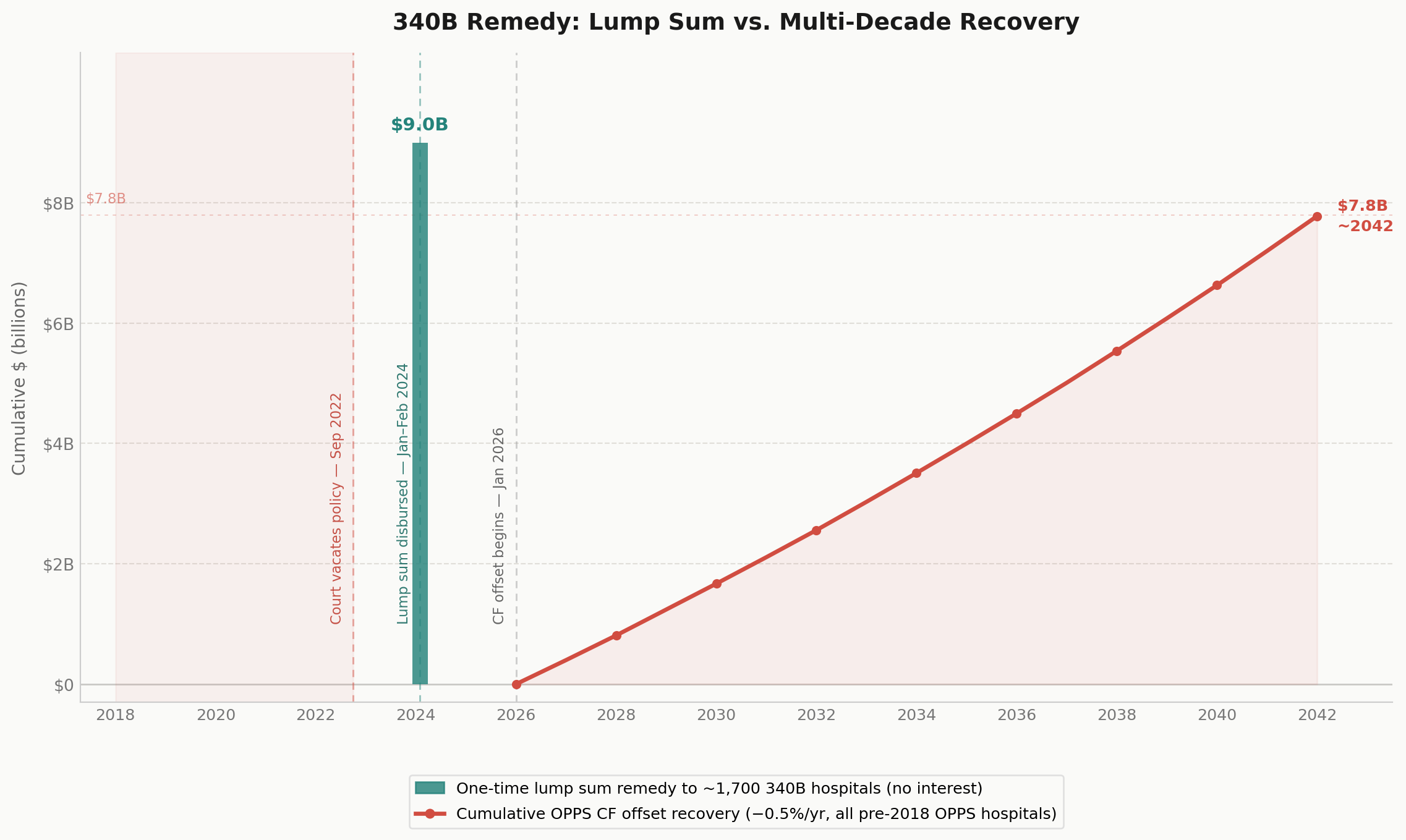

Five years of below-statutory payments left a $10.6 billion hole. Of that, $1.6 billion had already been recovered through claims reprocessing after the policy was vacated in late 2022 — leaving a net underpayment of $9.0 billion that CMS was obligated to remedy.

The Remedy Structure: The Conversion Factor Offset

Congress had not appropriated funds for this purpose. CMS had to design a remedy within its existing OPPS authority and recover the cost in a way that preserved budget neutrality. The CMS 340B Final Remedy Rule (CMS-1793-F), issued November 2, 2023, established two tracks.

The remedy payment: CMS instructed Medicare Administrative Contractors to disburse lump sum payments to approximately 1,700 affected 340B covered entity hospitals starting January 8, 2024, with all payments expected no later than February 7, 2024. No interest was included — CMS determined it lacked statutory authority to pay it. Non-340B hospitals received no remedy payment, because they were never subject to the ASP-22.5% cut.

The cost recovery mechanism — the conversion factor offset: To fund the remedy without exceeding OPPS budget authority, CMS reduces the OPPS conversion factor for non-drug items and services by 0.5% per year. The conversion factor is the multiplier that translates APC relative weights into dollar payment amounts for every non-drug, non-device OPPS service. The 0.5% annual reduction applies to all OPPS hospitals enrolled before January 1, 2018, and continues until the cumulative reduction equals $7.8 billion — a timeline that runs approximately through 2041 at the current rate.

The Asymmetry Worth Underscoring

The cost recovery mechanism is broad by design: 0.5% applies to every pre-2018 OPPS hospital’s non-drug service revenue regardless of 340B status. A 340B hospital absorbs that annual reduction but also received the lump sum remedy; whether the net is positive or negative depends on each hospital’s drug volume relative to its non-drug OPPS revenue mix. A non-340B hospital absorbs the offset with no remedy — a straight reduction to non-drug service revenue as the cost of remedying a wrong it did not participate in. This potential compounds with the site-neutral repricing from my previous post, which lands on the same income statement line through an entirely different statutory channel.

CY2027: The Rate, the Survey, and What Comes Next

The rate

CMS held the CF offset at 0.5% for CY2026. In the proposed rule, CMS had floated 2%; the final rule deferred that increase but stated explicitly that 2% would likely begin in CY2027. The difference between the two rates is not incremental. At 0.5% annually, a program reaches 2.5% cumulative compression after five years. At 2%, it reaches 10% in the same window — a planning problem of a different order.

The survey

The CY2026 final rule did something beyond setting the offset rate. Acting on a direct instruction from President Trump’s April 2025 executive order on drug pricing, CMS introduced the OPPS Drug Acquisition Cost Survey — a mandatory data collection requiring covered entities to report net acquisition cost, inclusive of all rebates and discounts, for specified covered outpatient drugs purchased between July 1, 2024 and June 30, 2025. CMS has stated the results will inform CY2027 rulemaking. This is the first OPPS rulemaking cycle to include an actual acquisition cost survey. Every prior year’s rate-setting — including the 2018 cut — proceeded without one.

That distinction matters because of what the Supreme Court established in AHA v. Becerra. The Court did not prohibit CMS from cutting 340B drug payment rates. It said CMS could only deviate from the statutory ASP+6% default after conducting exactly this kind of survey. CMS lacked that predicate in 2018; the Court blocked the cut on that basis alone. The survey now closes the statutory gap. Once CMS has the data, it has both the legal authority and — given the executive order and the explicit CMS commentary in the CY2026 final rule — the stated policy intent to act on it. The CY2026 rule, in other words, did not just set a rate. It built the foundation for a larger one.

Non-response is not a neutral option. CMS indicated it will impute the lowest acquisition cost reported among similar responding hospitals for any non-respondent — making declining to participate an actively adverse choice rather than a way to stay out of the data.

What comes next

The CY2027 proposed rule, typically released in late July, will be the first rule with both the legal authority and the empirical basis to reprice 340B drug payments. The CF offset rate — 0.5% or 2% — is one decision. What CMS does with the survey data on drug payment rates is another, potentially larger one. For programs with significant 340B drug volume, neither is a routine regulatory filing.

A Program in Transformation: The Rebate Model Debate

The acquisition cost survey is one front in a broader debate about whether the 340B program’s fundamental mechanics should be restructured.

The manufacturers claim that the upfront discount model is poorly targeted, prone to duplicate discounts where both 340B and Medicaid best price apply to the same dispensing, and has scaled into a program whose financial benefits are increasingly detached from patient need. They propose a rebate model where covered entities would receive an upfront payment at WAC, submit claims data documenting eligible dispensing, and receive manufacturer rebates based on verified patient-level attribution. The mechanism is designed to make eligibility visible and eliminate the conditions that produce duplicate discounts.

The hospital argue thatthe rebate model shifts cash flow risk onto entities that currently depend on upfront discounts to fund operations, adds administrative friction, and is structurally designed to shrink the program rather than reform it. The American Hospital Association argued in its April 2026 comment letter to HRSA that the switch would do “serious, irreparable harm to 340B hospitals and the patients they serve.”

The Trump administration launched a 340B Rebate Model Pilot Program in 2025 covering a limited set of drugs from eight manufacturers. That pilot was blocked by a federal court in February 2026 in American Hospital Association v. Kennedy, and HRSA restarted the process with a new request for information whose comment period closed April 20, 2026. The litigation has not resolved the underlying question; it has deferred it.

What this adds up to: the 340B program is simultaneously under pressure on three fronts — the CF offset compressing non-drug OPPS revenue, a likely CY2027 attempt to reprice 340B drug payments on the basis of the new survey, and a structural reform debate over the program’s discount mechanics that is actively in litigation. A covered entity with a significant drug program cannot treat any of these as routine.

Good Intentions, Complicated Consequences

Both policies in this series started from defensible premises. The site-of-service premium exists because Medicare built two billing tracks that reward care routing through hospital classification rather than clinical reality — site-neutral payment is the correction. The 340B program exists because safety-net providers need a structural cross-subsidy to serve populations that Medicare and Medicaid rates alone cannot adequately fund. The remedy is legally required because CMS overstepped its statutory authority. None of these are hard to defend in isolation.

The unintended consequences follow from the implementation. A safety-net subsidy scaled into an $81 billion procurement mechanism, with eligibility extended through the same acquisition dynamics that drove the site-of-service premium. A remedy financed by a broad-based offset that falls on every OPPS hospital regardless of whether they benefited. Blunt tools applied to structural design problems that the tools were not built to solve.

A more coherent system design would move toward a single reimbursement price for equivalent services regardless of facility classification, and toward a drug acquisition framework that links pricing to actual cost rather than preserving a margin structure that has grown beyond its original rationale. Neither is achievable through rulemaking alone. Both require Congressional action — the kind that has remained out of reach for decades and is unlikely to arrive soon. In its absence, CMS will keep working within the constraints of its existing authority: incremental, layered, and producing the kind of interacting policy changes that are genuinely difficult to track and price.

These changes arrive staggered, through different statutory channels, landing differently depending on site type, 340B status, and enrollment history. An MA plan on a three-year contract cycle, a VBC program benchmarked against prior-year FFS spend, a CFO building a five-year capital plan — none of them can model the combined effect without reliable, centralized data. That is where CMMI has a role beyond model design: building the data infrastructure and transparency that lets non-government institutions — actuaries, APM designers, operators — make data-informed decisions and meaningfully shape policy. Provider classification crosswalks, policy change logs, acquisition cost survey data made publicly available for independent analysis. The government sets the rules; democratizing access to the underlying data is what makes it possible for everyone else to keep up.

Key sources

American Hospital Association v. Becerra, 596 U.S. 724 (2022)

Executive Order, Lowering Drug Prices By Once Again Putting Americans First, April 15, 2025

Baker Donelson, Important Issues for 340B Providers in the OPPS Final Rule, December 2025

CMS OPPS Drug Acquisition Cost Survey Draft Template (CMS-10931)

American Hospital Association, Comment Letter on HRSA 340B Rebate Model RFI, April 20, 2026